A few months ago, I came across the story of Subedar (Retd.) Rajesh Kumar (name changed for privacy). He served the Indian Army with dedication for more than Three decades. After retirement, he continued using his old defence salary account for his pension credits, assuming everything would remain the same. Unfortunately, he never requested the bank to change it into a Defence Pension Account (DPA).

One unfortunate evening, Rajesh Kumar met with an accident on the highway and passed away. When his wife and children approached the bank to claim Personal Accidental Insurance (PAI)—a benefit available under the Memorandum of Understanding (MoU) between the Army and various banks—they were shocked. The bank refused their claim.

The reason? His account was still registered as a salary account, not as a pension account. Because of this technicality, the family lost lakhs of rupees that could have helped them during one of the darkest times of their lives.

This is not an isolated case. Many reports have been reaching Army Headquarters and the Directorate of Indian Army Veterans (DIAV). Families of retired personnel are losing out on rightful benefits because of one simple oversight: not converting a Defence Salary Account into a Defence Pension Account at the time of retirement.

DSP Account Full Form – Defence Salary Package Account

A Defence Salary Package (DSP) Account is a customised bank account offered to serving armed forces personnel with exclusive facilities like zero balance, free accidental insurance, concessional loans, and MoU-linked benefits. After retirement, it must be converted into a Defence Pension Account (DPA); otherwise, pensioners and their families may lose critical entitlements, including insurance coverage and financial security.

The Official Advisory

On 04 February 2025, the Adjutant General’s Branch, Integrated HQ of MoD (Army) issued a clear advisory (Tele: 351-12, B/27087/Advisory/AG/PS-3(P)) on this matter. The advisory highlights:

- Numerous cases are being reported where retired personnel have failed to convert their salary accounts into pension accounts.

- This leads to non-mapping of the account to the respective bank’s pension codes.

- As a result, pensioners are deemed ineligible for certain benefits linked to Defence Pension Accounts, including Personal Accidental Insurance (death/disability cover).

- Banks do not automatically know when a soldier retires, so it is the responsibility of the individual pensioner to inform the bank and request the conversion.

- Without this step, the soldier’s family—his Next of Kin (NoK)—may suffer huge financial losses in case of accidental death or disability.

Why Does This Happen?

Many soldiers believe that since their pension is being credited to the same account, everything is fine. But that’s a dangerous assumption. Banks categorize accounts differently:

- Salary Account → Active while in service, mapped to “defence salary” codes.

- Pension Account → Required after retirement, mapped to pension codes, and linked to benefits under Army–Bank MoU.

If the account is not converted:

- The bank continues treating it as a salary account.

- Accident insurance benefits (which are often automatic with pension accounts) do not apply.

- Claims for insurance or related facilities get rejected.

What Do You Lose If You Don’t Convert?

Failing to convert your account doesn’t just mean a small error—it could mean losing access to important protections. Some of the things at stake:

- Personal Accidental Insurance (PAI): This can be up to several lakhs, provided in case of accidental death or disability.

- Special Army–Bank MoU Benefits: Many banks give additional facilities to defence pensioners.

- Financial Security for Family: The NoK may lose crucial financial support during emergencies.

In short, what seems like a minor administrative task can become a life-altering mistake for your loved ones.

Whose Responsibility Is It?

The advisory makes it crystal clear:

- It is not automatic. Banks cannot know when a soldier retires.

- It is your duty. The retiring personnel must personally inform the bank.

- One visit can save your family. By submitting a simple request and a copy of your PPO (Pension Payment Order), your salary account can be converted into a pension account.

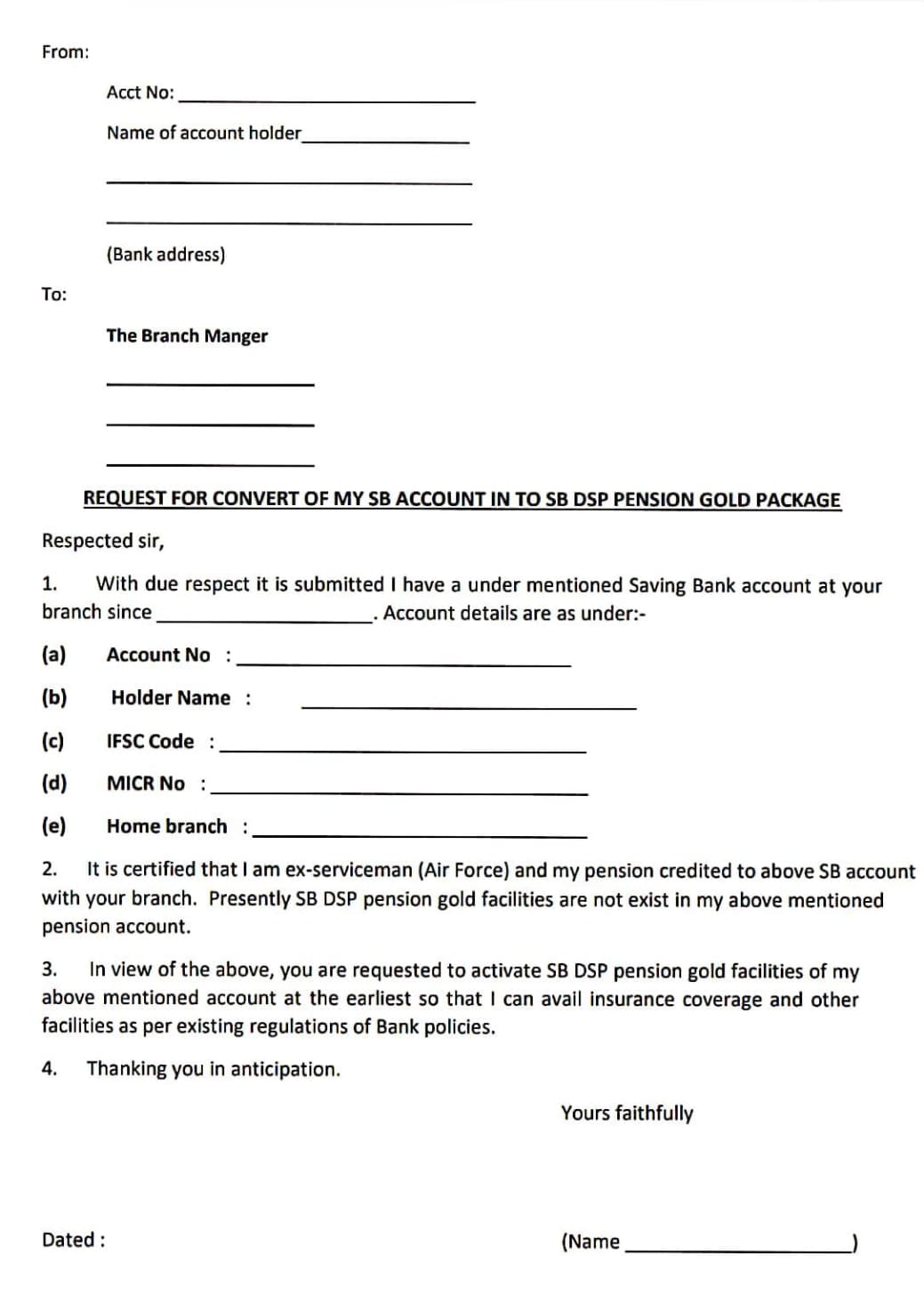

Steps to Change Your Defence Salary Account into a Pension Account

The process is simple, but you must take it seriously. Here’s a step-by-step approach:

- Approach the branch of the bank that holds your salary account.

- Submit a written request to convert it into a pension account.

Click here to Download form for converting DSP Salary Account to Defence Pension

{kind=link}

- Provide your PPO (Pension Payment Order) issued after retirement.

- Confirm the account is now tagged as a Defence Pension Account in the bank’s system.

- Ask about MoU-linked benefits, especially accidental insurance, and keep records.

A Message to Serving Personnel

If you are still in service, don’t ignore this advisory thinking it’s too early. Note down this requirement and share it with your course-mates, unit buddies, and family members. Many veterans admitted later, “Had someone told me earlier, I would have avoided this loss.”

Your awareness today could save your family from financial hardship tomorrow.

A Message to Veterans

If you have already retired and are not sure whether your account has been converted, take action immediately. Walk into your bank and ask. Taking a moment to recheck is always wiser than facing future loss.

The Bottom Line

The Army Headquarters has issued this advisory not as a routine circular but as a life-saving reminder. The story of Subedar Rajesh Kumar’s family is a harsh reality many others have faced. Don’t let your family be next.

Converting your account takes just a few minutes at the bank, but it safeguards your family’s future in ways you may not realize until tragedy strikes.

So next time you meet a retiring colleague, a veteran friend, or even think about your own retirement, remember:

Ensure your Defence Salary Account is converted into a pension account after retirement.

It’s not paperwork—it’s protection for your loved ones.

Read more l SBI DEFENCE SALARY PACKAGE ACCOUNT – FEATURES & BENEFITS EXPLAINED